CORRESP: A correspondence can be sent as a document with another submission type or can be sent as a separate submission.

Published on August 23, 2019

Know

Labs, Inc.

August

23, 2019

Mr.

David Burton, Accounting Branch Chief

Securities

Exchange Commission

Division

of Corporation Finance

Office

of Electronics and Machinery

1100

F Street N.E.

Washington, D.C. 20549

|

Re:

|

Know Labs, Inc.

|

|

|

Registration Statement on Form S-1

|

|

|

Filed May 30, 2019

|

|

|

File No. 333-231829

|

Dear

Mr. Burton,

Reference

is made to the Staff’s comment letter dated July 31, 2019

(the “Staff’s Letter”) to Know Labs, Inc. (the

“registrant” or “Company”). The registrant

hereby submits the following responses to the comments contained in

the Staff’s Letter with respect to the registrant’s

Registration Statement on Form S-1 filed with the SEC on May 30,

2019.

For

convenience of reference, each comment contained in the

Staff’s Letter is reprinted below, numbered to correspond

with the paragraph numbers assigned in the Staff’s Letter,

and is followed by the corresponding response of the registrant.

These comments have been made in response to the Staff’s

comments.

Registration Statement on Form S-1 filed May 30, 2019

Fee table, page i

1.

We note your

response to prior comment 2 and Exhibit A to your response. Given

that it appears that you are seeking to register the resale of

common shares, not the exercise of warrants or the conversion of

the preferred stock, it is unclear why your reliance on Rule 457(g)

is appropriate. Please clarify or revise as appropriate. Also: show

us how you calculated the "Proposed Maximum Aggregate Offering

Price" and "Amount of Registration Fee" for the shares of common

stock underlying the interest on the convertible notes; and tell us

how you determined the number of shares issuable upon exercise of

the Series F Preferred Warrants, given your disclosure on pages

32-33 regarding the number of warrants issued.

Response. The registration includes the registration of

resale of common shares underlying the notes, warrants and

preferred stock. We have revised our filing accordingly as set

forth in Exhibit A attached hereto and incorporated herein

by reference to remove reference to 457(g) in agreeance with the

Staff’s letter.

Further,

the "Proposed Maximum Aggregate Offering Price" and "Amount of

Registration Fee" for the shares of common stock underlying the

interest on the convertible notes was calculated by multiplying the

principal of the 8% Unsubordinated Convertible Notes ($2,242,515)

by the interest rate (8%) for the one year maturity of the note

bring the total interest to $339,401. The total interest was

multiplied by closing average ($1.53). We recognize there was an

error in the amount of shares to be registered underlying the

interest in and the proposed maximum offering price;

500

Union St. #810 Seattle WA 98101

Knowlabs.co

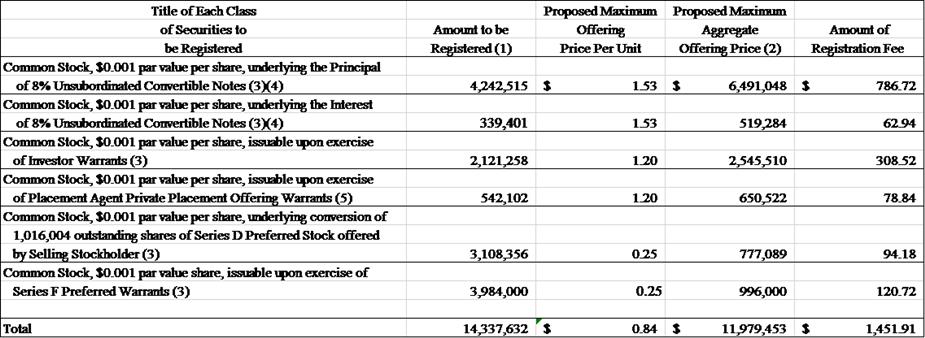

The fee

table has been revised it as follows:

|

Title of Each Class

|

|

Proposed

Maximum

|

Proposed

Maximum

|

|

|

of Securities to

|

Amount to be

|

Offering

|

Aggregate

|

Amount of

|

|

be Registered

|

Registered (1)

|

Price Per

Unit

|

Offering Price

(2)

|

Registration Fee

|

|

Common

Stock, $0.001 par value per share, underlying the

Interest

|

|

|

|

|

|

of

8% Unsubordinated Convertible Notes (3)(4)

|

339,401

|

1.53

|

519,294

|

62.94

|

With

respect to the number of shares issuable upon exercise of the

Series F Preferred Warrants (“Series F Warrants”),

given our disclosure on pages 32-33 regarding the number of

warrants issued. The Series F Preferred Warrants were calculated

based on the number of shares issuable upon the exercise of the

Series F Preferred Warrants multiplied by the funds the Registrant

will receive upon the exercise of the Series F Preferred

Warrants.

The

Registrant issued the following Series F warrants:

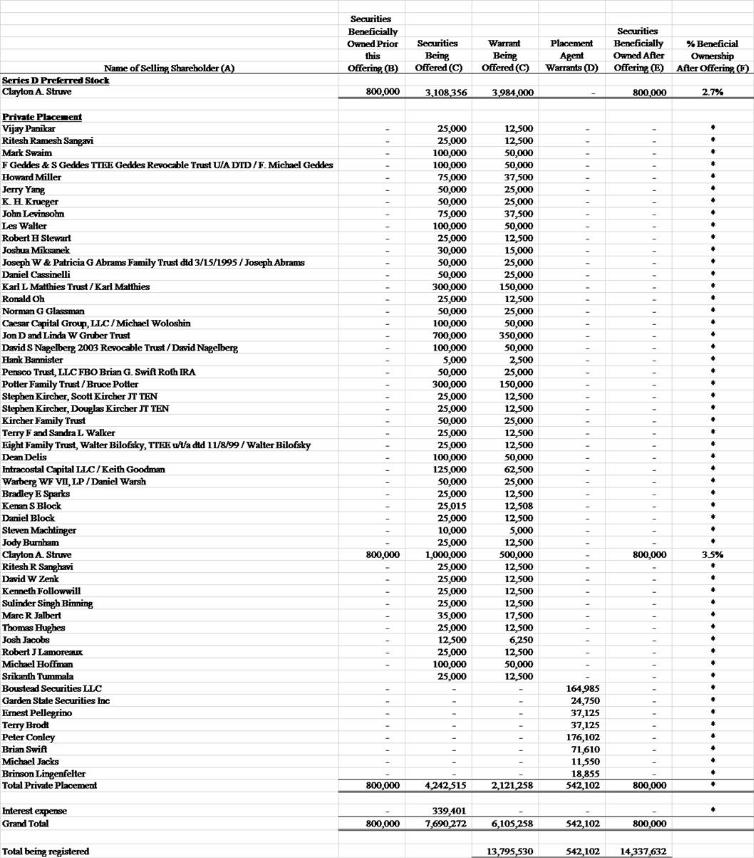

Selling Security Holders, page 30

2.

Please expand your

response to the second bullet point of prior comment 3 to address

the common stock issuable upon exercise of the Series F Preferred

Warrants.

Response. We are registering 3,984,000 shares of common stock issuable upon conversion of

outstanding Series F Warrants that were previously issued to one of

the Selling Shareholders in connection with Preferred Stock and

Warrant Purchase Agreement dated November 10, 2016 (the

“Purchase Agreement”). The Series F Warrants were

originally issued at an exercise price of $0.80, a slight discount

to market, however, due to certain protective provisions in the

Purchase Agreement, if certain securities of the Company were

issued at a price lower than $0.80 then the exercise price of the

Series F Warrants was to be adjusted downwards to match resulting

in a reduced exercise price of $0.25.

3.

Please disclose the

substance of your response to the fourth bullet point of prior

comment 3. Also disclose, if true, that all securities offered by

an affiliate of a broker-dealer were purchased by the seller in the

ordinary course of business, and, at the time of the purchase of

the securities to be resold, the seller had no agreements or

understandings, directly or indirectly, with any person to

distribute the securities.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

Response. All securities offered by the Broker-Dealer

Parties were received as compensation for underwriting activities

and were validly earned pursuant to their agreement with the

Company dated November 6, 2018 (the “Agreement”).

Pursuant to the Agreement, which is attached hereto as Exhibit B

and will be filed as an exhibit to Form S-1, Boustead Securities,

LLC a FINRA member, acted as our exclusive placement agent. They

received a 8% cash fee and 8% in warrants which are exercisable for

5 years at an exercise price of $1.20. All securities offered by an

affiliate of a broker-dealer were acquired by the seller in the

ordinary course of business, and, at the time of the purchase of

the securities to be resold, the seller had no agreements or

understandings, directly or indirectly, with any person to

distribute the securities.

4.

We note your

response to the eighth bullet point of prior comment 3. Please

ensure that the number of shares registered for sale in the fee

table is consistent with the shares listed in "Selling Security

Holders." We note in this regard that the "Grand Total" in column

(c) does not appear to reconcile to the proposed revisions to the

fee table.

Response. We have

revised the Selling Security Holders table, Grand Total in column C

to reconcile with the revisions to the fee table. We have included

a copy of the revised table as Exhibit B attached hereto and

incorporated herein by reference.

5.

We note from your

response to the tenth bullet point of prior comment 3 that the

company is not aware of any short positions held by any of the

selling stockholders. Please clarify whether that response was

based on information obtained from the Selling

Shareholders.

Response. The Company’s

response that is not aware of any short positions is based on its

reliance upon the contractual representations of the Selling

Shareholders as set forth in the Registration Rights Agreements

provided by each of the Selling Shareholders, a copy of which was

filed with the Registration Statement as Exhibit 10.33, which,

includes but is not limited to the following

representations:

“Company

has advised each Selling Shareholder that it is the view of the

Commission that it may not use shares registered on the

Registration Statement to cover short sales of Common Stock made

prior to the date on which the Registration Statement is declared

effective by the Commission, in accordance with 1997 Securities and

Exchange Commission Manual of Publicly Available Telephone

Interpretations Section A.65. If a Selling Shareholder uses the

prospectus for any sale of the Common Stock, it will be subject to

the prospectus delivery requirements of the Securities Act. The

Selling Shareholders will be responsible to comply with the

applicable provisions of the Securities Act and Exchange Act, and

the rules and regulations thereunder promulgated, including,

without limitation, Regulation M, as applicable to such Selling

Shareholders in connection with resales of their respective shares

under the Registration Statement.”

6.

Please expand your

response to prior comment 3 to provide us your analysis supporting

your conclusion regarding why your agreements with Boustead

Securities need not be filed as exhibits to your registration

statement.

Response. We do not disagree

and have filed a copy of the agreement with Boustead Securities as

Exhibit B, attached hereto and incorporated herein by reference,

and will file the same as an exhibit to our Form S-1

amendment.

7.

From your response

to prior comment 3, it appears that you do not intend to use cash

to repay the principal and interest under the note. It therefore

remains unclear whether in substance the transaction is a primary

offering of your common stock. Please expand your response, citing

all authority on which you rely, or revise your registration

statement as appropriate.

Response. The Company

respectfully submits that (i) the offering to be registered

pursuant to the Registration Statement is a valid secondary

offering and may be registered as contemplated by the Registration

Statement, and (ii) the Selling Security Holders are not

“underwriters” within the meaning of Section 2(a)(11)

of the Securities Act of 1933, as amended (the

“Securities

Act”).

500

Union St. #810 Seattle WA 98101

Knowlabs.co

Rule 415 Analysis

The

Staff has previously recognized the complexity of the analysis of

certain transactions under Rule 415 and has set forth a detailed

analysis of the relevant factors that should be examined in its

Compliance and Disclosure Interpretation (the “C&DI”)

612.09:

“It is

important to identify whether a purported secondary offering is

really a primary offering, i.e., the selling shareholders are

actually underwriters selling on behalf of an issuer. Underwriter

status may involve additional disclosure, including an

acknowledgment of the seller’s prospectus delivery

requirements ... The question of whether an offering styled a

secondary one is really on behalf of the issuer is a difficult

factual one, not merely a question of who receives the

proceeds. Consideration

should be given to how long the selling shareholders have held the

shares, the circumstances under which they received them, their

relationship to the issuer, the amount of shares involved, whether

the sellers are in the business of underwriting securities, and

finally, whether under all the circumstances it appears that the

seller is acting as a conduit for the issuer.” (emphasis added)

As

C&DI 612.09 indicates, the question is a

“difficult” and “factual” one that involves

an analysis of many factors and “all the

circumstances.” Each of the relevant factors listed in

C&DI 612.09 is discussed below. The Company respectfully

submits that, based on a proper consideration of all of these

factors, the Registration Statement relates to a valid secondary

offering and that all of the shares of Common Stock can be

registered for resale on behalf of the Selling Shareholders

pursuant to Rule 415.

How Long the Selling Shareholders Have Held the Shares

The

Company advises the Staff that the Selling Shareholders have now

held the securities, pursuant to which the underlying common stock

is being registered, as follows:

(i) all

securities associated with the offering and sale of the 8%

Unsubordinated Convertible Notes, including common stock underlying

the Principal and Interest of the Notes, the Warrants and Placement

Agent Warrants (collectively the “Note Offering”),

which were sold in a series of closings

between February 15, 2019 and May 28, 2019, have been held

for between nearly three (3) and five (5) months, and have not yet

effected any conversion of such securities into shares of Common

Stock.

(i) The

Selling Shareholder of the Series D Preferred Stock and Series F

Warrants (collectively the “Preferred”) acquired the

securities pursuant to the Preferred

Stock and Warrant Purchase Agreement dated November 10, 2016 and

has held the securities for nearly 3 years (the “Preferred

Offering”).

Presumably,

the longer securities are held, the less likely it is that the

Selling Shareholders are acting as a mere conduit for the issuer.

Since the time the Selling Shareholders acquired the securities,

they have had market risk. Moreover, there is currently no market

for the Preferred Stock nor the Notes or Warrants, and one is not

anticipated to develop. In addition, the earliest that the

investors or the Company can convert the Preferred and Notes into

Common Shares, for which there is a readily available market

(albeit, as discussed below, one with limited trading volume), is

one year after issuance (although the Notes could be mandatorily

converted earlier if the Company consummates Qualified Financing).

In addition, each Selling Shareholder made specific representations

to the Company that such investor was acquiring the respective

Notes and Preferred in the ordinary course of business for such

Selling Shareholders’ own account and not with a view

towards, or for resale in connection with, the public sale or

distribution thereof. None of the Selling Shareholders’ has

sold any of the Preferred nor Notes, and there is no evidence to

suggest that the representations made by the Selling

Shareholders’ are false. The fact that the Common Stock is

now being registered for resale is not evidence that the Selling

Shareholders desire to effect an immediate distribution, which in

fact the Selling Shareholders are not able to do given that the

Preferred Shares are not yet convertible into Common

Shares.

In

C&DI 116.19, the Staff codified its “PIPEs”

interpretation, which contemplates that a valid secondary offering

could occur immediately following the closing of a PIPE

transaction. C&DI 116.19 provides in relevant

part:

500

Union St. #810 Seattle WA 98101

Knowlabs.co

In

a PIPE transaction, a company will be permitted to register the

resale of securities prior to their issuance if the company has

completed a Section 4(2)-exempt sale of the securities (or in

the case of convertible securities, of the convertible security

itself) to the investor, and the investor is at market risk at the

time of filing of the resale registration statement….The

closing of the private placement of the unissued securities must

occur within a short time after the effectiveness of the resale

registration statement.

Furthermore,

it is important to note that C&DI 139.13 provides that no

minimum holding period is required where a company has completed a

private transaction of all of the securities it is registering and

the investor is at market risk at the time of filing of the resale

registration statement. The Company is not aware that the Staff has

taken the position that the period of time elapsing between closing

and registration has raised concerns about whether the offering is

a valid secondary offering. In fact, the Company believes that such

concerns would be inconsistent with C&DI 116.19. Because no

holding period is required for a PIPE transaction to be a valid

secondary offering, the period that has already elapsed since the

signing of the Purchase Agreements is substantially longer than the

holding period required by the Staff for valid PIPE transactions.

This concept comports with longstanding custom and practice in the

PIPEs marketplace.

The Circumstances under Which They Received the Shares

The

Company respectfully submits that registration for resale of the

shares of Common Stock issuable upon conversion of the Note

Offering should not equate to intent to distribute by Selling

Shareholders. The securities comprising the Note Offering were

issued pursuant to the Form of Securities Purchase Agreement,

Subscription Agreement, Convertible Note, Warrant, Subordination

Agreement, and registration Rights Agreement, were filed as

Exhibits 10.28-10.33 to the registrants S-1 filed May 30, 2019

(collectively the “Note Offering Purchase Agreements”).

The Preferred were issued pursuant to the Form of Preferred Stock

and Warrant Purchase Agreement, Registration Rights Agreement and

Form of Warrant, which were filed as Exhibits 10.1-10.3 to the

registrants S-1 filed May 30, 2019 (the “Preferred Purchase

Agreement”, and collectively with the Note Offering Purchase

Agreements, the “Purchase Agreements”).

The

securities acquired pursuant to the Purchase Agreements were issued

pursuant to

the exemption from registration provided by Section 4(a)(2) of

the Securities Act and/or Rule 506 of Regulation D promulgated

thereunder. Accordingly, the securities held by the Selling

Shareholders are, and at all times have been, restricted securities

that could not have been, and may not be, offered or sold in the

United States absent registration or an applicable exemption from

the registration requirements of the Securities Act. In the

Purchase Agreements, the Selling Shareholders made specific

representations to the Company that they were purchasing the

securities for their own accounts and not with a view to the resale

or distribution thereof, and that they had no present intention of

selling or otherwise distributing such securities. In addition,

each of the Selling Shareholders represented that it had made its

own independent decision to purchase securities in the private

placement. The Company is not aware of any evidence that would

indicate that these specific representations were

false.

No

Selling Shareholder, by virtue of the Note Offering and Preferred

Offering, has any other subscription rights to obtain additional

Common Stock shares. All of the Selling Shareholders were, have

continued to be, and will likely continue to be for some time, at

market risk with respect to their Notes and Preferred and the

Common Stock issuable upon conversion thereof.

In most PIPE transactions, including the Note

Offering and Preferred Offering, a registration statement is

required to be filed shortly after closing (typically 30 to 90

days) and declared effective shortly thereafter. Although the

Selling Shareholders bargained for registration rights as part of

the Note Offering and Preferred Offering, registration rights, in

and of themselves, do not evidence intent on the part of the

Selling Shareholder to sell the securities. The Company notes that

there are many reasons why investors prefer to have their

securities registered other than to effect an immediate sale,

including, but not limited to: (i) some private investment

funds are required to mark their portfolios to market and if

portfolio securities are not registered, such investors are

required to mark down the book value of those securities to reflect

an illiquidity discount and (ii) not registering the

securities would prevent investors from taking advantage of market

opportunities or from liquidating their investment if there is a

fundamental shift in their original investment determination about

the Company. In addition, some of

the Selling Shareholders are fiduciaries for their

trusts/beneficiaries; as a result, such Selling Shareholders have a

duty to act prudently. Accordingly, the Company understands that

the Selling Shareholders wish to have their securities in a more

liquid form, whereas not registering the securities could prevent

them from taking advantage of market opportunities or from

liquidating their investment if there is a fundamental shift in

their investment judgment about the Company.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

There

is no evidence that a distribution would occur if the Registration

Statement is declared effective. Under the Commission’s own

rules, a distribution requires “special selling

efforts”. Rule 100(b) of Regulation M defines a

“distribution” as “an offering of securities,

whether or not subject to registration under the Securities Act,

that is distinguished from ordinary trading transactions by the

magnitude of the offering and the presence of special selling

efforts and selling methods.”

Accordingly,

the mere size of a potential offering does not make a proposed sale

a “distribution.” Special selling efforts and selling

methods must be employed before an offering can constitute a

distribution. In this case, there is no evidence that any special

selling efforts or selling methods have or would take place if all

of the Common Shares issuable upon conversion of the Preferred and

Note Offerings and covered by the Registration Statement were

registered. To the Company’s knowledge, no Selling

Shareholder has any agreements or understandings, directly or

indirectly, with any person to distribute its securities, nor is

there any evidence that any of the Selling Shareholders have

conducted any road shows or taken any other actions to condition or

“prime” the market for their Shares. To do so would

violate the detailed representations made by them in the Purchase

Agreements.

The

circumstances of the Note and Preferred Offerings underscore that

it would be virtually impossible for the Selling Shareholders to

effect an illegal distribution even if they desired to do so

because the existing trading market for the Common Stock could not

absorb all of the Common Stock that may be issued to the Investors

upon conversion. According to the website Yahoo! Finance, the

three-month average daily trading volume of the Common Shares on

the OTCQB as of August 19, 2019 was approximately 13.99k shares. As

a result, it would take the Selling Shareholders nearly two years

to sell all of Common Stock shares subject to the Registration

Statement assuming no one else sold a single share. Furthermore,

the Selling Stockholder owning the Preferred Stock and warrants is

subject to a 4.99% blocker and as such may be even more limited in

the ability to sell the Common Stock shares subject to the

Registration Statement. In these circumstances, it is not credible

to conclude that the Selling Shareholder have purchased the

securities for the purpose of making a distribution. In this

situation, which is common in many PIPE transactions, the concept

that the Selling Shareholders have “freely tradable”

Shares is more theoretical than real. For all practical purposes,

the Investors are largely locked into their investments for a

significant period of time, regardless whether the common stock

underlying their securities are registered.

Selling Shareholders’ Relationship to the

Company

As disclosed in the Registration Statement, the

Selling Shareholders had no relationship with the Company prior to

its investment in the Notes Offering, with the exception of Clayton

Struve, who has invested in the past and is the sole Selling

Shareholder under the Preferred Offering. The Selling Shareholders

have no current relationship other than as a passive investor

holding the securities that have been issued to it.

None of the

Selling Shareholders are an affiliate of the Company. The Selling

Shareholders are not represented on the board of directors of the

Company, and the Selling Shareholders have no contractual rights to

control or otherwise influence the conduct of the Company’s

business and operations.

In

investor questionnaires delivered by the investors to the Company

in connection with the Purchase Agreements, each of the Investors

represented that it was not a broker-dealer registered with the

Commission. A handful of the Selling Shareholders are registered

brokers who received their warrants as consideration for services

rendered in the Notes Offering. As discussed above, each of the

Selling Shareholders also represented and warranted in the Purchase

Agreements that the securities being acquired by it were being

acquired for such Investor’s own account, not as nominee or

agent, and not with a view to the resale or distribution of any of

such securities in violation of the Securities Act. The Notes

Offering and Preferred Offering was negotiated at arm’s

length, with each of the Selling Shareholders incurring all of the

economic and market risk attendant to this type of

transaction.

In

fact, the Selling Shareholders are responsible for paying any

broker-dealer fees or underwriting discounts or commissions

directly to any broker-dealers they engage to assist in selling any

of the Company’s securities. The Selling Shareholders will

retain all proceeds from the sale of the securities pursuant to the

Registration Statement, and the Company will not obtain any direct

or indirect benefit from any amounts received from those sales. The

only exception being in the event a Selling Shareholder exercises a

warrant on a non-cashless basis.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

The

registration rights granted to the Selling Shareholders are

traditional registration rights and are not indicative of any

present intention of the Selling Shareholders to sell or distribute

the Common Stock, much less sell or distribute the Common Stock on

behalf of the Company. The decision to exercise these registration

rights now and request that the Common Shares be registered with

the Commission was made solely by the contractual obligations

promised to the Selling Shareholders. From the point of view of the

Company, filing the Registration Statement entails significant

legal, accounting and printing costs and filing fees with no

offsetting monetary benefits to the Company. Absent the Selling

Shareholders’ contractual registration rights, the Company

would not be filing the Registration Statement, and the Company

will not receive any proceeds from any subsequent sale of the

Common Shares. The Selling Shareholders negotiated the customary

registration rights set forth for a variety of business reasons,

and, in any case, the registration rights were not granted by the

Company for the purpose of conducting an indirect primary

offering.

The Amount of Shares

Involved

Assuming

all of the 14,337,632 Common Shares being registered for sale by

the Selling Shareholders under the Registration Statement are

issued, on an after-issued basis, they will represent approximately

39% of the total Common Shares outstanding (or approximately 54% of

the total Common Shares outstanding held by non-affiliates) based

on the number of Common Shares outstanding as of June 30,

2019.

The

Company acknowledges the large number of Common Shares involved.

While it appears that the number of Common Shares being registered

is a factor that the Staff considers in its determination regarding

whether an offering should be deemed a primary or secondary

offering, a single-minded focus on the number of securities is

inconsistent with C&DI 612.09 and the facts and circumstances

recited above. As described below, the Staff’s focus on

“toxic” features—which are not a factor in the

proposed offering—is far more likely to deter abusive

practices and uncover disguised primary offerings than a focus on

the number of securities being registered.

We

understand that several years ago the Staff became increasingly

concerned about public resales of securities purchased in

“toxic” transactions. The Staff believed that public

investors often did not have an appropriate understanding as to the

nature of the investment being made or the negative impact that

such transactions could have on the market prices of the shares

involved. In many of these “toxic” transactions, an

issuer would commit to issuing shares at a conversion price that

floated and was subject to change in accordance with the market

price of the underlying common stock. When the deals were

announced, the stock prices typically fell, resulting in the

issuance of significant blocks of stock. In these toxic situations,

existing investors or investors who purchased shares after the

announcement of the transaction frequently faced unrelenting

downward pressure on the value of their investments. In too many of

these cases, the shares held by non-participants in these

transactions were ultimately rendered worthless.

In

order to combat the effects of these toxic transactions, we

understand that the Office of the Chief Counsel and the senior

Staff members of the Commission’s Division of Corporation

Finance began to look at ways to discourage toxic transactions and

to limit the impact of these transactions. One way to do so was to

limit the ability of the investors in those transactions to have

their shares registered.

We

understand that, in order to monitor these types of transactions,

the Staff compared the number of shares an issuer sought to

register with the number of shares outstanding and held by

non-affiliates as disclosed in the issuer’s most recent

Annual Report on Form 10-K. As we understand it, the Staff was

instructed to look more closely at any situation where an offering

involved more than approximately one-third of the public float. If

an issuer sought to register more than one-third of its public

float, the Staff was instructed to examine the transaction to see

if it implicated Staff concerns that a secondary offering might be

a “disguised” primary offering for Rule 415 purposes.

However, according to the Office of the Chief Counsel, the test was

intended to be a mere screening test and was not intended to

substitute for a complete analysis of the factors cited in C&DI

612.09. Moreover, we understand that the Staff’s focus

shifted in late 2006 to “extreme convertible”

transactions to avoid disrupting legitimate PIPE transactions. As

described above, the terms of the Note Offering and Preferred

Offering do not implicate any of the concerns leading to the focus

on extreme convertible situations. There is no danger that public

investors do not have an appropriate understanding as to the nature

of the investment being made or any negative impact on the market

prices of the shares involved, as the Note Offering and Preferred

Offering have been fully disclosed in the Company’s filings

with the Commission.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

Furthermore,

focusing solely on the number of shares being registered in

relation to the shares outstanding or the public float has a

disproportionate impact on the ability of smaller public companies

to utilize the shelf registration process to register shares for

resale, thereby severely limiting their options to raise

funds.

If

the Staff’s concern is that a distribution is taking place,

the number of Shares being registered should be given less weight

in the Staff’s analysis. The availability of Rule 415 depends

on whether the offering is made by Selling Shareholders or deemed

to be made by or on behalf of the issuer. In order for the Staff to

determine that the offering is in fact on behalf of the issuer, by

definition the Staff must conclude that the Selling Shareholders

are seeking to effect a distribution of Shares. Clearly, an illegal

distribution of Shares can take place when the amount of Shares

involved is less than one-third of an issuer’s public float.

In fact, it is far easier to effect an illegal distribution when

the number of Shares involved is relatively small in relation to

the Shares outstanding or the public float. When investors acquire

a large stake of a small public company, particularly one with a

limited trading market like that of the Company, it is virtually

impossible for them to exit their equity position in an orderly

manner through the public markets.

Limiting

the number of Shares being registered does not effect any

significant change in the circumstances of a proposed offering. If

the Selling Shareholders are acting as a mere conduit for the

Company, cutting back on the number of Common Shares being sold

does not change the investment intent of the Selling Shareholders

or the ability of the Selling Shareholders to effect a distribution

if, in fact, that was their intent.

The

Staff’s interpretative position set forth in C&DI 612.12

makes clear that the amount of securities offered, whether by an

affiliate or otherwise, is not the determinative factor when

considering whether an offering is properly characterized as a

primary offering or a secondary offering. Other factors discussed

in this letter, such as the Selling Shareholders’ investment

intent, and the circumstances under which the Selling Shareholders

acquired the securities, support the characterization of the

proposed offering as secondary in nature. C&DI 612.12 describes

a scenario where a holder of well over one-third of the outstanding

stock is able to effect a valid secondary offering. The

interpretation states, in relevant part, that:

A

controlling person of an issuer owns a 73% block. That person will

sell the block in a registered “at-the-market” equity

offering. Rule 415(a)(4) [which places certain limitations on

“at-the-market” equity offerings] applies only to

offerings by or on behalf of the registrant. A secondary offering

by a control person that is not deemed to be by or on behalf of the

registrant is not restricted by Rule 415(a)(4).

In addition, C&DI 216.14, regarding the use of Form S-3 to

effect a secondary offering provides:

Secondary

sales by affiliates may be made under General Instruction I.B.3. to

Form S-3 [relating to secondary offerings], even in cases where the

affiliate owns more than 50% of the issuer’s securities,

unless the facts and circumstances indicate that the affiliate is

acting as an underwriter or by or on behalf of the

issuer.

These interpretive positions support the Company’s belief

that a holder of well in excess of one-third of the public float

can effect a valid secondary offering of its Shares unless other

facts—beyond the mere level of ownership—indicate that

the holder is acting as a conduit for the issuer.

A

focus on the number of shares being registered appears reminiscent

of the “presumptive underwriter” doctrine, under which

the Staff previously took the position that the sale of more than

10% of the outstanding registered stock of an issuer made the

investor a “presumptive underwriter” of the offering.

The Company notes that the presumptive underwriter doctrine was

abandoned by the Staff more than 20 years ago. See American Council

of Life Insurance (avail. June 10, 1983). More recent rule

making has continued this trend away from this doctrine. See

Securities Act Release No. 33-8869 (December 6, 2007)

(eliminating the “presumptive underwriter” provisions

of Rule 145(c) and (d) in most cases). Accordingly, the

Company believes that there is no basis to apply the doctrine

here.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

A

focus solely on numbers of Common Shares to be registered also

ignores a fundamental aspect of these transactions: investors in

PIPEs are funding business plans and strategic initiatives, not

looking to take control of public issuers or to illegally

distribute Shares. In this case, the investors evaluated an

investment in the Company on the basis of the business purpose for

the Note Offering and Preferred Offering and whether they believed

that the Company’s proposed use of proceeds was rational and

likely to produce above average investment returns. By focusing on

the percentage of the public float or the percentage of the Shares

outstanding, the Staff unfairly penalizes smaller companies such as

the Company by disproportionately hindering their ability to raise

desperately-needed capital to execute their business plans and

strategic initiatives. It is difficult to harmonize a focus on the

number of securities being registered by smaller companies with the

Commission’s public commitment to smaller companies.

Furthermore, the enactment of the Jumpstart Our Business Startups

Act demonstrates that Congress is focused on making access to the

capital markets easier, not harder, for smaller public

companies.

Indeed,

as indicated in its periodic reports, the Company’s ability

to grow and develop is technology and products, requires the

completion of financings, such as the one represented by the Note

Offering and Preferred Offering, in a timely manner. Investors like

the Selling Shareholders provide issuers like the Company with the

means to further their business plans and strategic initiatives

and, by extension, to provide returns to all Stockholders. In the

case of the Note Offering and Preferred Offering, the Investors

evaluated an investment in the Company on the basis of the business

purpose for the offering and whether they believed the

Company’s use of proceeds was rational and likely to produce

favorable investment returns. The number of shares that they

purchased was simply a mathematical result of the size of the

investment, the price per unit and the Company’s market

capitalization. PIPE investors do not typically look to acquire a

specific proportion of a company and then calculate an investment

amount based on that desired level of ownership. We respectfully

submit that cutting off the ability to finance the operations of

smaller companies through transactions such as the Private

Placement will create dire consequences for these types of

companies and their investors, with no corresponding benefit from

an investor protection perspective or otherwise.

Whether the Sellers Are in the

Business of Underwriting Securities

Aside

from the Broker-Dealer Parties, who hold warrants received as

compensation for services, none of the Selling Shareholders has an

underwriting relationship with the Company or, to the

Company’s knowledge, is in the business of underwriting

securities. The Selling Shareholders buy and sell securities for

their own accounts and not for the accounts of others. All of the

Selling Shareholders represented at the time of purchase that they

were buying for their own accounts and not with an intention to

distribute in violation of the Securities Act. There is no

allegation that those representations and warranties are untrue and

no factual basis exists for any such allegation. To the

Company’s knowledge, none of the Selling Shareholders has

sold any of the securities being registered since the closing of

the respective offering, nor have any Selling Shareholders

converted the Notes or Preferred shares. In addition, to the

Company’s knowledge, no Selling Shareholders has any

agreements or understandings, directly or indirectly, with any

person to distribute the Common Stock issuable upon conversion of

the Notes or Preferred shares.

Section 2(a)(11)

of the Securities Act defines the term “underwriter” as

“any person who has purchased from an issuer with a view to,

or offers or sells for an issuer in connection with, the

distribution of any security, or participates or has a direct or

indirect participation in any such undertaking, or participates or

has a participation in the direct or indirect underwriting of any

such undertaking….” Each Selling Shareholder has

represented that such Selling Shareholder has purchased the

securities convertible into the Common Shares in the ordinary

course for such Selling Shareholder’s own account and not

with a view toward, or for resale in connection with, the public

sale or distribution thereof, except pursuant to sales registered

under the Securities Act or under an exemption from such

registration and in compliance with applicable federal and state

securities laws, and they do not have a present arrangement to

effect any distribution of the Common Shares registered in the

Registration Statement to or through any person or entity.

Accordingly, the Company believes that none of the characteristics

commonly associated with acting as an underwriter are

present.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

Whether Under All the

Circumstances it appears that the Selling Shareholders are Acting

as a Conduit for the Issuer

As

the facts and analysis provided above demonstrate, the Selling

Shareholders are not engaging in a distribution and are not acting

as conduits for the Company. The Selling Shareholders made

fundamental decisions to invest in the Company, have held their

securities for a period of time that exceeds the periods sanctioned

in the Staff’s C&DIs, and have represented that they

purchased the securities for their own accounts and not with a view

to the resale or distribution thereof, and that they had no present

intention of selling or otherwise distributing such securities. In

addition, each of the Selling Shareholders represented that it had

made its own independent decision to purchase the securities, and

there is no evidence to suggest that any of the Selling

Shareholders are acting in concert to effect a coordinated

distribution of the securities.

None

of the Selling Shareholders are in the business of underwriting

securities and all of the proceeds of the offering of the Common

Shares under the Registration Statement will be retained by the

Selling Shareholders. In these circumstances, the Company believes

that the offering it seeks to register pursuant to the Registration

Statement is a valid secondary offering that should be allowed to

proceed consistent with Rule 415.

Conclusion

For

all of the foregoing reasons, the Company believes that the facts

and circumstances compel the conclusion that the offering pursuant

to the Registration Statement is a valid secondary offering by the

Selling Shareholders eligible to be made on a shelf basis under

Rule 415(a)(1)(i) and that the Company should be permitted to

proceed with the registration of all of the Common Shares issuable

in connection with the conversion of the Notes and Preferred issued

pursuant to the Note Offering and Preferred Offering. No potential

violation of Rule 415 exists and, in these circumstances, there is

no risk to the investing public if the Registration Statement is

declared effective as to all of the Common Shares issuable in

connection with the Private Placement.

8.

Please

include in your response to prior comment 3 information regarding

prior securities transactions between the issuer (or any of its

predecessors) and the Selling Shareholders, any affiliates of the

Selling Shareholders, or any person with whom any Selling

Shareholder has a contractual relationship regarding the

transaction (or any predecessors of those persons). Include the

date of each transaction and the consideration paid, and whether

the securities have since been sold by the Selling Shareholder.

Also clearly identify in your response when you have previously

registered securities for resale by the selling security holders

named in this registration statement, including whether and when

those securities have been sold.

Response. There are no prior

securities transactions between the Company and the selling

shareholders or affiliates or contractual parties thereto with

exception of those following parties and transactions described in

Exhibit C attached hereto and incorporated herein by

reference.

In furtherance to the information provided in Exhibit C, the only

securities set forth therein which have been registered are (i)

1,785,714 shares of common stock issuable upon conversion of the

Series C Redeemable Convertible Preferred Stock and (ii) up to

1,785,714 shares of common stock issuable upon the exercise of

outstanding Series E Warrants. These were registered via Form S-1

as amended by Post Effective Amendment made effective August 21,

2018. No shares have been sold by the Selling Shareholder.

The

9.

Please disclose (1)

the price of your common stock on the dates that the selling

security holders acquired the offered common stock or the

securities by which they can acquire the offered common stock, and

(2) the cash fee paid to the selling security holder. Also: clarify

how the conversion and exercise price adjustments will be made for

events requiring adjustments; and in the context of your disclosure

regarding the Series D Convertible Preferred Stock, disclose the

stated value of that preferred stock.

Response. (1) The Price of the

Company’s common stock on the date the Selling Shareholders

acquired securities

by which they can acquire the offered common stock was as follows:

(i) the offering price of the 8% convertible notes, warrants and

related securities issued between January 31, 2019 and May 2019,

was set at approximately $1.00 per share which was the closing

price of the Company’s common stock as of January 31, 2019

(the date the offering commenced). The average closing stock price

between January 31, 2019 and May 31, 2019 was approximately $1.57,

and (ii) the Series D Preferred Stock and Series F Warrants were

acquired on November 10, 2016 at a stated value of $0.80 per share;

the closing price of the common stock on the date before the

agreement was executed was $1.33 per share.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

(2)

(i)With the exception of the $361,401 fee paid to Boustead

Securities and their affiliates or assign, no cash fee was paid to

the Selling Shareholders owning the 8% convertible notes, warrants

and related securities; (ii) no cash fee has been paid to the

Selling Stockholder owning the Series D Preferred Stock and Series

F Warrants.

(3) The

8% notes and warrants will be adjusted proportionately in the event

of dividends, splits, or other reclassifications. With respect to

the conversion and exercise price adjustments for events requiring

adjustments, pursuant to Section 5(a) of the Series D Preferred

Stock, the conversion price will be adjusted proportionately in the

event of dividends in shares, stock splits, or other

reclassifications, and pursuant to Section 5(b) will be adjusted

downwards to match a conversion, exchange or exercise price per

share offered by the Company to another party which is less than

the Conversion Price of the Series D Preferred immediately in

effect prior to such sale or issuance. The stated value of the

Series D Preferred Stock is currently $0.70 per share.

Please contact me at (206) 903-1351 with any

questions.

Sincerely,

/s/ Ronald P. Erickson

Chairman of the

Board

cc: Kevin Kuhar, Securities and Exchange

Commission

Tim

Buchmiller, Securities and Exchange Commission

Russel

Mancuso, Securities and Exchange Commission

Jessica

M. Lockett, Esq.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

EXHIBIT

A

CALCULATION OF REGISTRATION FEE

(1) In

the event of a stock split, stock dividend or similar transaction

involving our common stock, in order to prevent dilution, the

number of shares registered shall be automatically increased to

cover the additional shares in accordance with Rule 416(a) under

the Securities Act of 1933, as amended (the “Securities

Act”).

(2)

Calculated pursuant to Rule 457(o) based on an estimate of the

proposed maximum aggregate offering price and specifically using

the price at which the warrants may be

exercised.

(3)This

Registration Statement covers the resale by our selling

shareholders (the "Selling Shareholders") of:

(i)up

to 4,242,515 shares of common stock underlying the conversion of

principal amount of registrants 8% Unsubordinated Convertible Notes

(“Principal Shares”)

(ii)up

to 339,402 shares of common stock issuable by the registrant

upon the conversion of interest accrued under the 8%

Unsubordinated Convertible Notes (“Interest Shares”)

(The Principal Shares and Interest Shares are referred to

collectively as the “Shares”).

(iii)

up to 2,121,258 shares (the "Investor Warrant Shares") of common

stock issuable upon the exercise of outstanding investor's warrants

(the "Investor Warrants") at an exercise price of $1.20 that were

previously issued to the Selling Shareholders in connection with 8%

Unsubordinated Convertible Notes offering that closed in a series

of closings between February 15, 2019 and May 28,

2019.

(v) up

to 3,108,356 shares of common stock underlying the outstanding

Series D Convertible Preferred Stock which is convertible at any

time at an initial conversion price of $0.25 per share of our

common stock subject to adjustment for certain events

(“Series D Shares”). There are currently 3,108,356

common shares estimated to underlying the 1,016,004 issued and

outstanding Series D Shares.

(vi) up

to 3,984,000 shares of common stock issuable upon conversion

of outstanding Series F Warrants at an exercise price of $0.25 per

share that were previously issued to one of the Selling

Shareholders in connection with Preferred Stock and Warrant

Purchase Agreement dated November 10, 2016 (“Series F Warrant

Shares”).

(4)

Estimated in accordance with Rule 457(c) of the Securities Act,

solely for the purposes of calculating the registration fee based

upon the average of the high and low prices as reported on the Over

the Counter Bulletin Board ("OTCBB") as of May 29,

2019.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

(5) We are registering 542,102 shares of our common stock issuable

upon the exercise of outstanding placement agent warrants (the

“Placement Agent Warrants”) at an exercise price of

$1.20 per share that were previously issued to Boustead Securities,

LLC and its assigns (collectively “Placement Agent”)

pursuant to an engagement agreement dated November 6, 2018 (the

“Boustead Offering Engagement Agreement”) which

provides that the Placement Agent shall receive that certain number

of warrants to purchase the common stock of the Company equal to

the number of warrants issued under the 8% Unsubordinated

Convertible Note Offering (the “Offering”). In the

event of stock splits, stock dividends or similar transactions

involving the common stock, the number of common shares registered

shall, unless otherwise expressly provided, automatically be deemed

to cover the additional securities to be offered or issued pursuant

to Rule 416 promulgated under the Securities Act of 1933, as

amended (the “Securities Act”). In the event that the

provisions of the agreements require the registrant to issue more

shares than are being registered in this registration statement,

for reasons other than those stated in Rule 416 of the Securities

Act, the registrant will file a new registration statement to

register those additional shares.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

EXHIBIT B

500

Union St. #810 Seattle WA 98101

Knowlabs.co

EXHIBIT

C

Garden State Securities, Inc.

The Company issued the following warrants for the issuance of

common stock to Garden State Securities, Inc. or its employees

related to the Clayton A. Struve transactions detailed

below.

Convertible Promissory Notes, Series C and D Preferred Stock and

related warrants- warrants for the purchase of 837,901 common

shares exercisable at $0.25 per share.

Private placement being registered- warrants for the purchase of

99,000 shares of common stock exercisable at $1.20 per

share.

None of the Garden State Securities, Inc. shares have been

previously registered. On March 28, 2019, 10,610 shares of common

stock were issued to an employee of Garden State Securities, Inc.

related to the exercise of a warrant.

Clayton A. Struve

The Company has engaged in transactions with Mr. Struve, the

Preferred D holder, since approximately 2016. The following is a

summary of transactions with Mr. Struve:

Convertible Promissory Note dated September 30, 2016

On September 30, 2016, the Company entered into a $210,000

Convertible Promissory Note with Clayton A. Struve, an accredited

investor of the Company, to fund short-term working capital. The

Convertible Promissory Note accrued interest at a rate of 10% per

annum and was due on March 30, 2017. The Note holder can convert

the Note into common stock at $0.70 per share. During the year

ended September 30, 2017, the Company recorded interest of $21,000

related to the convertible note. This note was extended in the

Securities Purchase Agreement, General Security Agreement and

Subordination Agreement dated August 14, 2017 with a maturity date

of August 13, 2018. Also, the conversion price of the Debenture was

adjusted to $0.25 per share, subject to certain adjustments. The

balance was increased $75,000 during the year ended September 30,

2018. On November 16, 2018, we signed Amendment 1 to Senior

Secured Convertible Redeemable Notes dated September 30,

2016extending the due dates of the Note to February 27, 2019. On

September 24, 2018, Mr. Struve converted $200,000 of the Note into

800,000 shares of our common stock. The Company recorded accrued interest of $54,671

as of September 30, 2018.

Series C and D Preferred Stock and Warrants

On

August 5, 2016, the Company closed a Series C Preferred Stock and

Warrant Purchase Agreement with Clayton A. Struve, an accredited

investor for the purchase of $1,250,000 of preferred stock with a

conversion price of $0.70 per share. The preferred stock has a

yield of 8% and an ownership blocker of 4.99%. In addition, Mr.

Struve received a five-year warrant to acquire 1,785,714 shares of

common stock at $0.70 per share.

To

determine the effective conversion price, a portion of the proceeds

received by the Company upon issuance of the Series C Preferred

Stock was first allocated to the freestanding warrants issued as

part of this transaction. Given that the warrants will not

subsequently be measured at fair value, the Company determined that

the warrants should receive an allocation of the proceeds based on

their relative fair value. This is based on the understanding that

the FASB staff and the SEC staff believe that a freestanding

instrument issued in a basket transaction should be initially

measured at fair value if it is required to be subsequently

measured at fair value pursuant to US generally accepted accounting

principles (“GAAP”), with the residual proceeds from

the transaction allocated to any remaining instruments based on

their relative fair values. As such, the warrants were allocated a

fair value of approximately $514,706 upon issuance, with the

remaining $735,294 of proceeds allocated to the Series C Preferred

Stock.

Proportionately,

this allocation resulted in approximately 59% of the face amount of

the Series C Preferred Stock issuance remaining, which applied to

the stated conversion price of $0.70 resulted in an effective

conversion price of approximately $0.41.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

Having

determined the effective conversion price, the Company then

compared this to the fair value of the underlying Common Stock as

of the commitment date, which was approximately $1.06 per share,

and concluded that the conversion feature did have an intrinsic

value of $0.65 per share. As such, the Company concluded that the

Series C Preferred Stock did contain a beneficial conversion

feature and an accounting entry and additional financial statement

disclosure was required.

Because

our preferred stock is perpetual, with no stated maturity date, and

the conversions may occur any time from inception, the dividend is

recognized immediately when a beneficial conversion exists at

issuance. During the year ending September 30, 2016, the Company

recognized preferred stock dividends of $1.16 million on Series C

preferred stock related to the beneficial conversion feature

arising from a common stock effective conversion rate of $0.41

versus a current market price of $1.06 per common

share.

On

November 14, 2016, the Company issued 187,500 shares of Series D

Convertible Preferred Stock and a warrant to purchase 187,500

shares of common stock in a private placement to certain accredited

investors for gross proceeds of $150,000 pursuant to a Series D

Preferred Stock and Warrant Purchase Agreement dated November 10,

2016.

The

warrants associated with the November 14, 2016 issuance were

allocated a fair value of approximately $56,539 upon issuance, with

the remaining $63,539 of net proceeds allocated to the Series D

Preferred Stock. Proportionately, this allocation resulted in

approximately 53% of the amount of the Series D Preferred Stock

issuance remaining, which applied to the stated conversion price of

$0.80 resulted in an effective conversion price of approximately

$0.34. Having determined the effective conversion price, the

Company then compared this to the fair value of the underlying

Common Stock as of the commitment date, which was approximately

$1.14 per share, and concluded that the conversion feature did have

an intrinsic value of $0.80 per share. As such, the Company

concluded that the Series D Preferred Stock did contain a

beneficial conversion feature of $150,211 which was recorded as a

beneficial conversion in stockholders’ equity.

On

December 19, 2016, the Company issued 187,500 shares of Series D

Convertible Preferred Stock and a warrant to purchase 187,500

shares of common stock in a private placement to an accredited

investor for gross proceeds of $150,000 pursuant to a Series D

Preferred Stock and Warrant Purchase Agreement dated December 14,

2016.

The

warrants associated with the December 19, 2016 issuance were

allocated a fair value of approximately $60,357 upon issuance, with

the remaining $69,643 of net proceeds allocated to the Series D

Preferred Stock. Proportionately, this allocation resulted in

approximately 54% of the amount of the Series D Preferred Stock

issuance remaining, which applied to the stated conversion price of

$0.80 resulted in an effective conversion price of approximately

$0.37. Having determined the effective conversion price, the

Company then compared this to the fair value of the underlying

Common Stock as of the commitment date, which was approximately

$0.81 per share, and concluded that the conversion feature did have

an intrinsic value of $0.44 per share. As such, the Company

concluded that the Series C Preferred Stock did contain a

beneficial conversion feature of $82,232 which was recorded as a

beneficial conversion in stockholders’ equity.

Because

the Company’s preferred stock is perpetual, with no stated

maturity date, and the conversions may occur any time from

inception, the dividend is recognized immediately when a beneficial

conversion exists at issuance. During the year ending September 30,

2017, the Company recognized preferred stock dividends of $2.3

million on Series D preferred stock related to the beneficial

conversion feature arising from a common stock effective conversion

rate of $0.34 and $0.37 versus the original market price of $1.14

and $1.06 per common share, respectively.

On May 1, 2017, the Company issued 357,143 shares of Series D

Convertible Preferred Stock and a warrant to purchase 357,143

shares of common stock in a private placement to an accredited

investor for gross proceeds of $250,000 pursuant to a Series D

Preferred Stock and Warrant Purchase Agreement dated May 1,

2016.

The initial conversion price of the Series D Shares is $0.70 per

share, subject to certain adjustments. The initial exercise price

of the warrant is $0.70 per share, also subject to certain

adjustments. The Company also amended and restated the Certificate

of Designations, resulting in an adjustment to the conversion price

of all currently outstanding Series D Shares to $0.70 per

share.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

On August 14, 2017, the price of the Series C and D Preferred Stock were

adjusted to $0.25 per share pursuant

to the documents governing such instruments. After adjustment there

were 3,108,356 shares of Series D preferred stock

authorized.

On July

17, 2018, the Company filed with the State of Nevada a second

Amended and Restated Certificate of Designation of Preferences,

Powers, and Rights of the Series D Convertible Preferred Stock. The

Amended Certificate restates the prior Certificate of Designation

filed on May 8, 2017 to decrease the number of authorized Series D

shares from 3,906,250 shares to 1,016,014 shares.

As of June 30, 2019, the Company has 3,108,356 of Series D

Preferred Stock outstanding with Clayton A. Struve, an accredited

investor, outstanding. On August 14,

2017, the price of the Series D

Stock were adjusted to $0.25 per share pursuant to the documents governing such

instruments.

Securities Purchase Agreement dated August 14, 2017

On August 14, 2017, the Company issued a senior convertible

exchangeable debenture with a principal amount of $360,000 and a

common stock purchase warrant to purchase 1,440,000 shares of

common stock in a private placement to Clayton Struve for gross

proceeds of $300,000 pursuant to a Securities Purchase Agreement

dated August 14, 2017. The debenture accrues interest at 20% per

annum and matures August 13, 2018. The convertible debenture

contains a beneficial conversion valued at $110,629. The warrants

were valued at $111,429. Because the note is immediately

convertible, the warrants and beneficial conversion were expensed

as interest.

On the same date, the Company entered into a General Security

Agreement with the Mr. Struve, pursuant to which the Company has

agreed to grant a security interest to the investor in

substantially all of our assets, effective upon the filing of a

UCC-3 termination statement to terminate the security interest held

by Capital Source Business Finance Group in the assets of the

Company. In addition, an entity affiliated with Ronald P. Erickson,

out then Chief Executive Officer, entered into a Subordination

Agreement with the investor pursuant to which all debt owed by us

to such entity is subordinated to amounts owed by us to Mr. Struve

under the Debenture (including amounts that become owing under any

Debentures issued to the investor in the future).

The initial conversion price of the Debenture is $0.25 per share,

subject to certain adjustments. The initial exercise price of the

Warrant is $0.25 per share, also subject to certain

adjustments.

As part of the Purchase Agreement, the Company granted the investor

“piggyback” registration rights to register the shares

of common stock issuable upon the conversion of the Debenture and

the exercise of the Warrant with the Securities and Exchange

Commission for resale or other disposition.

The Debenture and the Warrant were issued in a transaction that was

not registered under the Securities Act of 1933, as amended in

reliance upon applicable exemptions from registration under Section

4(a)(2) of the Act and Rule 506 of SEC Regulation D under the Act.

Under the terms of the Purchase Agreement, Mr. Struve may purchase

up to an aggregate of $1,000,000 principal amount of Debentures

(before a 20% original issue discount) (and Warrants to purchase up

to an aggregate of 250,000 shares of common stock). These

securities are being offered on a “best efforts” basis

by the placement agent.

During the year ended September 30, 2017, $156,941 was recorded as

interest expense related to debt discounts, beneficial conversions

and warrants associated with Convertible Promissory

Notes.

On December 12, 2017, the Company closed an additional $250,000 and

issued a senior convertible exchangeable debenture with a principal

amount of $300,000 and a common stock purchase warrant to purchase

1,200,000 shares of common stock in a private placement dated

December 12, 2017 with Mr. Struve pursuant to a Securities Purchase

Agreement dated August 14, 2017. The convertible debenture contains

a beneficial conversion valued at $93,174. The warrants were valued

at $123,600. Because the note is immediately convertible, the

warrants and beneficial conversion were expensed as

interest.

On March 2, 2018, the Company received gross proceeds of $280,000

in exchange for issuing a senior convertible redeemable debenture

with a principal amount of $336,000 and a warrant to purchase

1,344,000 shares of common stock in a private placement dated

February 28, 2018 with Mr. Struve pursuant to a Securities Purchase

Agreement dated August 14, 2017. The convertible debenture contains

a beneficial conversion valued at $252,932. The warrants were

valued at $348,096. Because the note is immediately convertible,

the warrants and beneficial conversion were expensed as

interest.

500

Union St. #810 Seattle WA 98101

Knowlabs.co

In connection with the February 28, 2018 private placement, the

placement agent for the debenture and the warrant received a cash

fee of $28,000 and the Company issued warrants to purchase shares

of the Company’s common stock to the placement agent or its

affiliates based on 10% of proceeds.

On

November 16, 2018, the Company signed Amendment 1 to Senior Secured

Convertible Redeemable Notes dated August 14, 2017 and December 12,

2017, extending the due dates of the Notes to February 27,

2019.

Convertible Promissory Notes with Clayton A. Struve

As of March 31, 2019, the Company owes Clayton A. Struve $1,071,000

under convertible promissory or OID notes. The Company recorded

accrued interest of $58,411 as of March 31, 2019. On May 8,

2019, the Company signed Amendment 2 to the convertible promissory

or OID notes, extending the due dates to September 30,

2019.

500

Union St. #810 Seattle WA 98101

Knowlabs.co